The Altcoin Bull Case

The Emotional Context

This article is a follow-up to a series of ideas around digital tokens we explored over the past 12 months and is likely our final say on the matter. We’ve already discussed historical token design shortcomings and followed it up with a proposed solution. It also accompanies our broader thesis on crypto/Web3: how macro-economic, social and technological trends shaping the world today provide strong tailwinds for decentralized technologies and digitally-native assets no short-to-mid-term obstacles can block. We believe the next wave of internet monopolies is likely to be decentralized and expect strong demand for censorship resistant software even if UI/UX is only on par with incumbents.

So having said so much on this topic, we almost feel forced to continue the conversation about why tokens are important and valuable at this point. But the industry sentiment towards them has shifted so dramatically lower recently (marking its bottom, in our humble opinion) and generally has changed so much since Ethereum introduced a wide investor base to ICOs 9 years ago - that we feel obliged to remind our readers that the original vision still has merit.

The “altcoin” market’s underperformance to Bitcoin and other asset classes in 2025 as well as the rise of stablecoin-based businesses pushed the debate around token value to a very emotionally charged set of arguments, unfortunately not as rich with substance. When talking to industry operators, it is clear most of them are looking past tokens and leaning towards traditional business models for their Web3 endeavours. And they’re pretty emotional about it too. It really feels like it’s over.

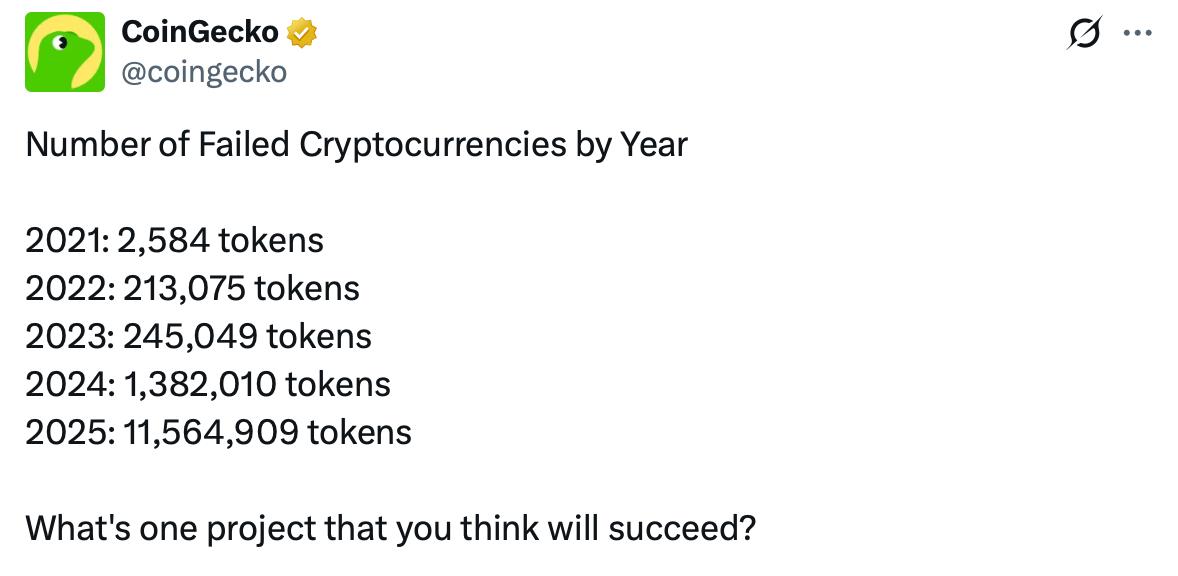

Source: X

Source: X

Most of the original big believers are disillusioned by now - having observed time and time again how issuers abuse their right of mint with absurd levels of deceit. Essentially, fraud has been industrialized and implicitly accepted in crypto - mostly pushed by multiple fund manager-founder-exchange-KOL cabals of insiders. And grift is penetrating higher and higher up those ranks as overall cynicism and disillusionment grows. The majority of insiders can no longer imagine better ways to use blockchains other than for various gambling wrappers: prediction markets, launchpads, perpetual futures exchanges. And since the prevailing view is that for everything else “there’s no utility”, people just issue tokens as a fundraising scheme and hope to make something off of the few naive buyers left (net of exchange and market maker “fees”, a.k.a. racket). These days an average founder sees their token almost exclusively as a fundraising tool and has no idea what makes people buy it other than naive expectations of quick riches, which they essentially leech off of.

However, when viewed without the gloomy cynicism surrounding tokens lately or the aura of naiveté of the “good ol’ days”, the topic is very timely – as the U.S. legislators are preparing to codify their treatment of digital assets. And we expect the rest of the world’s biggest jurisdictions to follow along more-or-less similar lines. These moves will usher in a new era of acceptance for digitally-native assets with clear legal incentives and responsibilities for founders to do right by their stakeholders.

While we’re bullish on the overall direction, we’d like to highlight why it’s important to stay true to the cypher punk ethos for us as investors and builders to get the biggest economic outcomes from this development.

The Factual Context

There are three recent news stories that broke out consecutively over the last quarter of 2025, all highlighting the growing trend of token neglect by even “serious” teams. Founders trying to distance their “real world” equity and actual value generated by their technology from community-owned “worthless” tokens. Although none of this is by any means new, becoming more explicit than ever is what makes it emblematic of the average Web3 builder’s mindset these days. We’ll provide very brief summaries below; it’s best the interested reader uses other sources for details.

1. Aave Labs vs Aave DAO

Internal conflict within the Aave community is a story that surfaced recently and TLDR from how we understood it: there’s a for-profit company, Aave Labs, that has essentially been the main organization contributing code to the Aave protocol, one of the longest-standing and largest DeFi products (lending); and this company has been trying to monetize the protocol without passing on those revenues back to the DAO, which is a non-legal but on-chain organization representing all the stakeholders of the $AAVE token.

In the most recent episode, Labs switched the swap feature on the frontend that produced revenue for the DAO to a different provider and had the revenue stream redirected to their own wallets, which sparked a community backlash. The two founders of Aave ended up on the two sides of the debate, which prompted an independent proposal to strip the Labs of rights to the Aave brand, control over main communication channels and domains (having a proper legal entity own these, as opposed to a DAO, was the original justification). The back-and-forth essentially ended in Lab’s favor, since the community abstained from taking decisive action in fear of $AAVE losing value, but still “broadly expressed its voice”.

To provide more context: Aave DAO has been covering Aave Lab’s costs for shipping new versions of the protocol (in millions of $USD) and has been contributing to the risk management and other core product features underlying the “opinionated” frontend shipped by the Labs team. Also, Aave started as an ICO project in 2017 that raised its initial proceeds in a public sale of the token – in total amounting to almost $17m. That’s what initially financed and jump-started the business of Labs.

Aave Labs (or affiliated entities) also holds one or more business licenses to operate a centralized fintech business on top of the protocol, and, as mentioned earlier, maintains control over the Aave IP (also originally paid for by the DAO) and plans to monetize it further with consumer products in the near future – since a decentralized group of wallets holding a digital token cannot do so legally.

2. Circle’s acquisition of Axelar protocol’s core team

A stablecoin issuer Circle that went public earlier in 2025, has acquired a private company called Interop Labs for their intellectual property and talent. This company, though, had a publicly traded token tied to its core product – Axelar Protocol - and there are no other significant contributors to it other than Interop Labs, although a standalone Foundation that had been setup to issue the token is still using Axelar communications channels on behalf of the “community”.

Moreover, there are reports of a private raise by the team not long ago via an over-the-counter sale of their tokens - $30m worth to private investors. We’re speculating, but most likely those token-derived funds were used to support the business of Interop Labs rather than the Foundation. Yet, token holders didn’t receive anything from the subsequent business sale. There was no signaling to token holders ahead of the acquisition by the team as well as no formal legal recourse after the fact.

The project is widely known as Axelar and this name and underlying technology encompass the intellectual property produced by Interop Labs to-date, as far as we understand. Most likely, the remaining Foundation will slowly wind down as their funding dries up and its “community” dissipates.

3. Coinbase’s acquisition of Vector

Another similar acquisition happened a few weeks earlier when Coinbase acquired a product (rather than the whole business) off of a Solana-based team that also had a publicly traded token with some quazi-equity mechanics.

The product, called Vector, is a transaction router business that earns trading fees by taking user order flow. It was the only successful unit in the overall enterprise named Terminal, which originally started as an NFT marketplace of the same name (still functional), with the team then shifting most of their focus to Vector.

The issue is exacerbated by the fact that the publicly traded $TRMNL token jumped ahead of the announcement, clearly signaling insider buying. But as it turned out, even insiders didn’t realize the acquisition meant nothing for the Terminal token holders.

The Question

So, all the above examples prompt the same question: what do token holders own and what rights do they have? Or posed more broadly: why do token sales fund businesses token holders never end up owning or having a real say over? As controversial as it may sound, we find the question redundant.

If one is to view tokens as an asset class representing specific legal rights codified outside of token mechanics, they would permanently lock themselves into the real-to-digital world imperfect loop that creates these collisions in the first place. Of course, we are certain that multiple digital tokens will be turned into equity-like assets (not to be mistaken with tokenized securities) and obtain defensible legal protections, just like other digital assets have in the past (e.g. IP). But we don’t find the prospect as compelling for token value proposition (and accrual) as it may appear on the surface.

By “equity-like” we mean that tokens will be treated as cashflow assets with rights similar to equities with the passing of Digital Asset Market Clarity Act in the U.S. (regardless of how long the recent fight over its final wording takes). We expect most other jurisdictions to follow the U.S. in principle, just as they did it for regulating equity or derivatives markets. So we think of these principles as a global regulatory environment for crypto rather than a U.S. phenomena, bar certain exceptions.

The rules will require corresponding disclosures from insiders, some “gradual decentralization” tests to reduce their burden over time and other well-intended, but consequentially restrictive measures. It’s the path of least resistance: adopting well-established legal frameworks, which in turn allow for established valuation methods to be applied to tokens and also let the market transparently price in management moves. However, the downside is multiple limitations over the longer term.

Primarily, if a token confers some legal rights to its holder, it, by definition, is bound by the applicability and defensibility of such rights in specific jurisdictions. In the world of at least next 10-15 years, where countries/regions are growing apart and are fighting military, trade and cyber wars - this is a bug, not a feature. As an issuer or contributor to such a project you may be restricted to service only regions you are allowed to by your primary jurisdiction (e.g. if you register as U.S.-based token issuer you may be restricted from serving Russian or Chinese customers). And while there will always be workarounds, one can hardly build internet-scale monopolies facing such barriers.

Besides potential global distribution and product coverage limitations, this framework will also incentivize revenue maximization. So far, the only projects with clear product-market-fit in Web3 are DeFi applications: lending, risk management, prediction and perpetual futures markets. They will have an easier time adapting to the new rules. However, most of the time their fee-based value capture is leaky relative to the overall value generated by the product. In a decentralized setting, besides the code developers, applications are often run with the help of independent service suppliers. Uniswap, the leading decentralized exchange, is a textbook example – most of the trading fees it generates go directly to liquidity providers to incentivize their participation in the Uniswap markets. So, while it sure is a very lean operation, leaky value capture may not seem as exciting to the market. Again, this limits decentralization incentives for founders: why have a community of independent protocol service suppliers when it eats into your margins?

Besides application-layer tokens, best suited for such an equity-like model, there are also infrastructure-layer ones (DePINs, L1s, middleware-tied digital assets, etc.). This subsector has been historically hard to price and even harder to generate consistent revenues with due to the price volatility of their tokens. A good example of this would be something like Filecoin, a decentralized storage cloud with the best underlying technology, where using it for storage is often unfeasible due to token-denominated pricing – regardless of how good the tech is. Any burst of adoption also caps it in the long run, as the service becomes overpriced. So, the “practical” equilibrium the market has found for such tokens is low adoption combined with expectation-based marketing to sustain the price in some manageable range while they slowly bleed out value due to structural flow imbalance favoring suppliers (e.g. storage providers in case of Filecoin), who are always net sellers.

Tokens of this kind may be the biggest casualty of the new legislation, even though they’re getting carved out as “digital commodities” - but only after passing a decentralization/maturity test which means that no one group of operators holds significant control over it. So, for the first few years of trading at least, tokens in this category will still be compared with more equity-like digital assets, and if the market doesn’t put any growth premium on their ability to generate revenue, their founders will be forced to seek “quick fixes” which probably result in centralization and abandonment of a token strategy altogether. This train of thought goes something like: 1) “Why incentivize third party providers of hardware with a token they keep selling to cover dollar-denominated costs if you can just pay them in dollars”. 2) “Incentivizing/subsidising third parties with (VC) dollars is more expensive than owning your own stack”. 3) “Users don’t want to pay in volatile tokens either, let's switch to charging them in dollars and let’s own our own hardware”. And this is how you end up with a traditional cloud business the original DePIN was launched to disrupt.

Thus, we strongly believe that the most “natural” answer to the posed question and mental framework giving birth to the question in the first place – i.e. can we provide token holders with the rights similar to those of equity holders - lead to a suboptimal economic outcome for Web3 businesses in the long run, because it likely reduces their ability to produce global-scale unstoppable services.

Is There Another Answer?

Before we offer some ideas as to how to overcome the limitations presented above, let us just summarize the factors described earlier:

- Most of the tokens so far have been used by founders as a fundraising tool and exclusively just that – primarily feeding on investors’ expectations. This couldn’t go on forever, even with the multiple shapeshifts the trend has taken over the years to sustain itself, the 9 year “worthless tokens” era is probably over – culminating in a meme coin bull run of ’23-’24 juxtaposed with a bunch of “VC coin” market blow outs. We believe that raising funds without “any explicit expectations of returns” or whatever the legal patch says to protect the issuers is much closer to financial fraud than some of them would like to believe.

- The world where token holders have equity-like rights is upon us and it’s no longer based on ethics (which always fail given incentives), but mostly law. We are expecting to see some combinations of equity-like rights (to profits and governance), maybe even mixed in with some utility for certain token types.

- That above option, if it is to become the primary model, is actually limiting to tokens’ censorship resistance and decentralization, since it directly puts founders and stakeholders within legal norms of jurisdictions that allow for and regulate issuance and turnover of such tokens. Whilst the change from existing frameworks may not seem as drastic, in reality U.S. leaning into letting token founders distribute the revenues their software generates, implies a stronger dependence on other U.S. regulations – including, for example, on countries/regions they are allowed to serve. We expect most other jurisdictions to follow along the same footsteps, creating regional/national Web3 ecosystems rather than global ones.

So, the natural conclusion and the fourth statement in this series should be: we also expect big jurisdictions to start competing for the sector by offering tax rebates, streamlined registration and the like - as part of a broader protectionist trend and emphasis on self-reliance in key industries. Given these legal restrictions wrapped as incentives, no token issuer will dare to decentralize and compete for global coverage unless they have the ability to do so without breaking the law.

But we already have a legal way of launching and contributing code to digital assets, established in multiple reputable jurisdictions like e.g. Switzerland: the founders can mint tokens to themselves and monetize (i.e. sell) them without ever touching/distributing user revenues. Also, there has been a legislative push, including in the pending Clarity Act, to separate developers’ code contribution from other activities like hosting a frontend, and more importantly - from what the code does. We’ve seen a similar interpretation in a recent high-profile court practice as well.

There’s a reason Ethereum is equally used by Larry Fink’s asset management team and Kim Jung Un’s hackers and no-one bats an eye! It is a decentralized platform after all and the fact that anyone can use its applications is bullish for $ETH, because they need to use the token to access it. This is a clear product-market-fit and you’d want to keep it that way, regardless of the pressures against it – because it’s exactly what makes Ethereum valuable versus e.g. AWS.

We won’t go into details about specific mechanics that token issuers may implement, because they are often project-specific. But briefly, it mostly involves automation+autonomy, where the token is an active component of the UX-flow or revenue flow of smart contracts that generate it. Mechanically tying the token with the core features of the product, or its revenue distribution (e.g. automation of fee collection towards token holders), or upgrades/governance. Essentially any contract can require an account interacting with it to hold a certain amount of token balance, or signal certain preference with those tokens, or spend a certain amount of tokens to it, etc. All of these and many more features can be embedded into existing and new applications. Developers just haven’t considered that the market may reward these with a higher premium, but as soon as someone does it to a revenue-generating product without harming its UX – the market will.

Our ideal Web3 product is a censorship resistant and autonomous set of smart contracts that can only be accessed through such a token, which is freely tradeable on chain. This mechanism also places the token at the gateway to the product and avoids any value leakage. We don’t expect the majority of Web3 services and products to switch to this model just yet. Neither do we push portfolio companies we help with token design to do so, but over time this is the model that makes most sense. Tying the product usage directly to a freely tradeable, globally accessible digital token is a powerful way to avoid any legal chokepoints and capture most value.

The Bull Case

So, to summarize: we are bullish on altcoins in general (short-to-mid-term) and the properly structured ones specifically (mid-to-long-term). The pending Clarity Act will usher in a new narrative and excitement about tokens, in our view. But over time it will also create structural limitations for issuers.

Yet our bull case is simple. Tokens that have the features and properties laid out in the previous section – primarily, close integration with the product, autonomy and resulting censorship-resistance, combined with most value accretive placement - will over time outperform the ones that don’t. Tokens’ defensibility over time, to which censorship resistance can contribute a lot, will become more and more important as software moats become obsolete in the world of vibe-coding and personalized agents.

What proponents of strict revenue-based token evaluation fail to realize is the digital space is not going to consistently build itself anew every generation. What future AI monopolies and hopefully some Web3 protocols (as a check on them) are fighting for is the dominance in their portion of the digital stack for decades to come. So, a censorship-resistant, common good-looking-like protocol or application, in our view, has a greater chance of maintaining their dominance/relevance for decades than a profit-maximizing company. And thus, multiples applied to such digital businesses should be higher. Hence the decentralization premium intuited by markets for e.g. $ETH and $SOL relative to their “revenues” is directionally correct, given potential decades-long durability of such revenue streams.

Not every internet protocol or app has to be a decentralized digital common good though, so Web2 and Web3 will probably co-evolve, albeit some Web2 apps shrinking in coverage (turning to regional champs instead of global). But crucial things like money, markets, compute and other digital commodities, data, digital “staples” (e.g. identity) and similar - will probably end up in the Web3 bucket.

So, as a builder one needs to think not about how to pump a worthless digital “memorabilia” to a $1bn market cap real quick, but how to build sustainable decades-proof digital networks powered by and coordinated with that one single asset that can amass trillions of dollars in value and have multi-generational impact. And some builders will. And it gets us incredibly bullish.