The New "Value Stack"

Some Context

It is common knowledge in traditional tech (both software and hardware) that a company that locks the “last mile” to the end customer usually captures most value in the value chain of the product. Last mile is also most competitive, so it still makes sense for risk averse founders to go down the value chain and produce intermediate components or services that make up the final product.

In the land of distributed technology businesses known as Web3 (or the Internet, ver. 3.0) - where intermediation is ideally minimized, ownership decentralized and services automated - it is easy to fall to a conclusion that such a value chain is inverted. The earliest infrastructure to run Web3 applications were the monoliths of Bitcoin and Ethereum, with each network having their respective paradigms (e.g. “the internet money” and “the internet computer”) for applications leveraging their openness. Thus, investors realized that the protocols themselves rather than applications on top of them may capture most of that value. This gave rise to the Fat Protocol Thesis.

This thinking still drives the majority of capital towards underlying infrastructure in Web3 such as so-called Layer 1s, 2s and even Layer 3s (or application-specific chains/rollups). Yet, the vision behind it has evolved from monolithic to more modular and thus spun out even more infrastructure startups to fund.

Since then, however, we’ve also seen applications emerge which have enjoyed significant benefits in reducing deployment and distribution costs by using Ethereum, while getting significant upside by issuing tokens that don't necessarily even capture the value the product generates (primarily due to regulatory concerns, which is temporary) . Uniswap is a prime example of this, even though they just finally started turning the fee switch on. While it was multiples off of Ethereum’s valuation even at peak, the cost of development and go-to-market speed for such an application is significantly lower than that of a competing Web2 online trading application, while it benefits from outsourcing large portion of operational costs to Ethereum validators and maintainers. It is a good business model.

So, of course, with the emergence of such apps the narrative shifted for some time, and many public and private market investments have flown into new super app contenders in Web3, primarily in Gaming and biggest TAM DeFi applications (e.g. liquid staking).

We’ve been thinking a lot about which mental framework would surface best Web3 business models that command the most value. This gave birth to our value stack thesis which currently guides our investment decisions and portfolio composition.

Forces that Shape the New Value Stack

We believe that two core trends will define the global technology sector. Starting in software and internet (which will become synonyms as security gaps between offline and online are closed), we expect those trends to then trickle down into the physical world over time.

The trends are:

- decentralization, driven by proliferation of public blockchains and blockchain-like (deterministic, trustless, censorship-resistant) distributed systems. It is a set of systems around any assets, first and foremost, including autonomous programs. We think of blockchain-like tech as "lassos" around e.g. AI, just as legal systems contained real-world violence when humanity shifted towards agriculture. This will lead to everything (first digital and then physical assets' "twins") going onto the Web. No need for on-premise setups and downloadable clients in the near future as scalability and bandwidth bottlenecks are inevitably resolved and blockchain-like crypto systems provide even better security while keeping everyone and everything connected;

- autonomous agents in both the digital and physical world, driven by proliferation of artificial intelligence and robotics. Machines will take up the absolute majority of the internet traffic and usage. We think the end state for consumer apps is a combination of highly customizable AI agent interfaces for things that are mundane; while the more creative and engaging ones probably end up as gamified experiences for human users while still maintaining a high AI component.

To reiterate: we think that most of business processes as well as our user experiences will be automated, while the parameters and preferences we set for them can remain in our verifiable control. Also, scalability limitations and complexity which are current bottlenecks for decentralized analogues of best Web2 products, will be resolved in the next 3 to 5 years, so we assume this to be taken care of by the time the thesis starts fully playing out.

This also means that we will end up with a very different value chain, because these technologies are by their nature global at scale. Everything will be online and interconnected. The major conclusion here is that the internet value stack will end up homogeneous across the globe.

In our view, the winning applications and protocols making it up will become global common goods managed and accessed via public blockchain-like distributed networks. There may be jurisdiction-specific rules and limitations around interacting with them, but it will still be (for the most part) the same stack.

What is the Value Stack

Let’s now explain what we mean by "the value stack" with an oversimplified example.

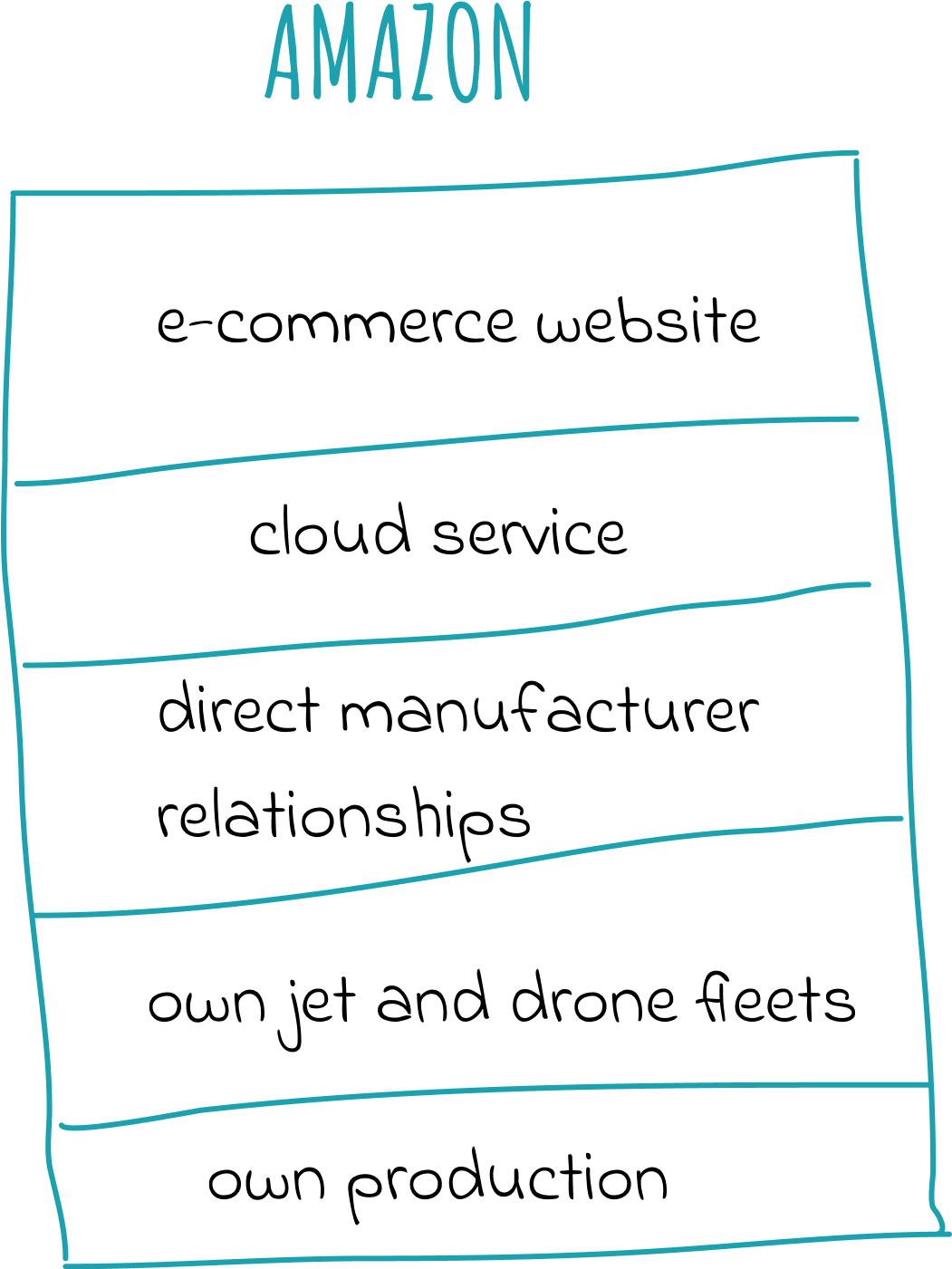

Amazon started out as an infinite store shelf first for books and then everything else – this was the last mile they captured. They were able to lock consumers in by providing and expanding the list of additional products to the original book offering. From having to just resell publishers they essentially became a publisher themselves over time, creating a platform for it via Kindle and later other content via Amazon Prime. But what really allowed them to reduce their costs and finally break into profitability was moving down the technology and value stack and selling access to their backend, which was idle 95% of the year other than during Christmas shopping. This gave rise to their cloud platform AWS. Also, in order to improve customer experience and grow new customers, which otherwise would have used brick-and-mortar shops, they had to go down the value creation chain further and build out delivery service that was exceptionally fast and ended up with the largest private fleet of airplanes and drones in the US. They also partnered with manufacturers to sell some of their most in-demand products under their own brand in order to keep the prices attractively low and maintain speed of delivery.

Simplified Amazon Value Stack

That’s in a nutshell how an e-commerce platform turns itself into a cloud and infrastructure and logistics company – by moving vertically down the value stack and owning it. From the last mile at the top all the way down to manufacturing in order to juice every ounce of profit margins and satisfy the customer. Of course, they also rely on common infrastructure like TCP/IP on the internet or concrete roads in the physical world, which also form that value chain - as many other things, which for simplicity can be left out. But to maintain dominance in their business, Amazon needs to own the vertical stack and has to do so over time after first locking in the main component that gives them actual growth factor. It is similar in varying degrees for other business giants.

Going down a value stack that makes up your main product is a much more natural process for a company than, say, expanding to adjacent or completely new markets, which they still always do, but with varying degrees of success. They always have a better chance to fully own the vertical value stack of their business rather than dominate horizontally (i.e. across multiple markets/jurisdictions/platforms). Owning portions of their value stack creates economies of scale and thus pushes off competition. Expanding to new markets is more risky and less clear-cut.

Regardless of how strong the vertical value stack is for Amazon in the US and other select regions, they cannot own it universally across the globe, so they either rely on partners who own e.g. better distribution in some specific region, or deal with competition in the form of businesses who own similar type vertical stacks in other regions and exert dominance there - like Alibaba in China. They may never be identical copies of each other, as e.g. Alibaba doesn't own any of the warehouses or logistics operations, but instead owns other portions of it's value chain (financial services via Alipay) to arrive at its local market dominance.

Regional Competition between Different Companies’ Vertical Value Stacks (Simplified)

So, the winning business model in traditional tech is growing the value stack vertically top-down to have widest profit margins possible and stave away competition. That still doesn’t save those businesses from being disrupted once in a while.

The Value Stack in Web3

We believe that winning Web3 protocols and applications will become globally accessible common goods for their specific use cases, as widest access usually creates a power law dynamic (with majority of people using 1 or 2 winning solutions). These distributed products are usually networks of either both service providers+users (e.g. Bitcoin) or just users (e.g. Uniswap). They are also by nature censorship resistant, "open for business" 24/7 and similarly open for anyone to contribute to them or build on top of them. There is no reason for both the users and contributors to not treat the winning solution as their go-to product for a certain use case given such an environment. Winners are most likely the ones that take most mindshare, liquidity and other network effects.

This also means that Web3 is made up of multiple applications and protocols, with each taking up a slice of this decentralized global value creation chain, but none owning it completely. Interoperability and openness command a certain level of specialization (depending on the field). In a world where everything is open source you need to be the absolute best or have the biggest network effects due to some other exceptional trait in your field. E.g. in a world where everything is open source you need to be the absolute best or have the biggest network effects due to some other exceptional trait in your field. Also, if you reduce interoperability functionality to enforce it, users will just pick a different solution that doesn't because that is where the value for them is. Finally you, still obviously can build your own full value stack, but the incentives are already skewed towards building on top of existing solutions rather than creating everything on your - the reduction in costs of setting up your protocol and distributing it to the widest group of users (wallets on the blockchain) is just too dramatic + the more contributors such open source technology has the more robust it becomes. It's an economic, cultural and thus social movement that is hard to reverse.

Expanding the metaphor of the value stack being made up of slices of technologies, vertically those value slices taken by specific apps or protocols may turn out much smaller/thinner (vertical value capture limited) for the reasons offered above. But the global nature of the markets Web3 creates allows such businesses to serve an audience multiples larger any region-winning player like Amazon or Alibaba could dream of. So horizontally such a slice may have a potential value capture "surface area" much larger than its Web2 analog still restricted by competition.

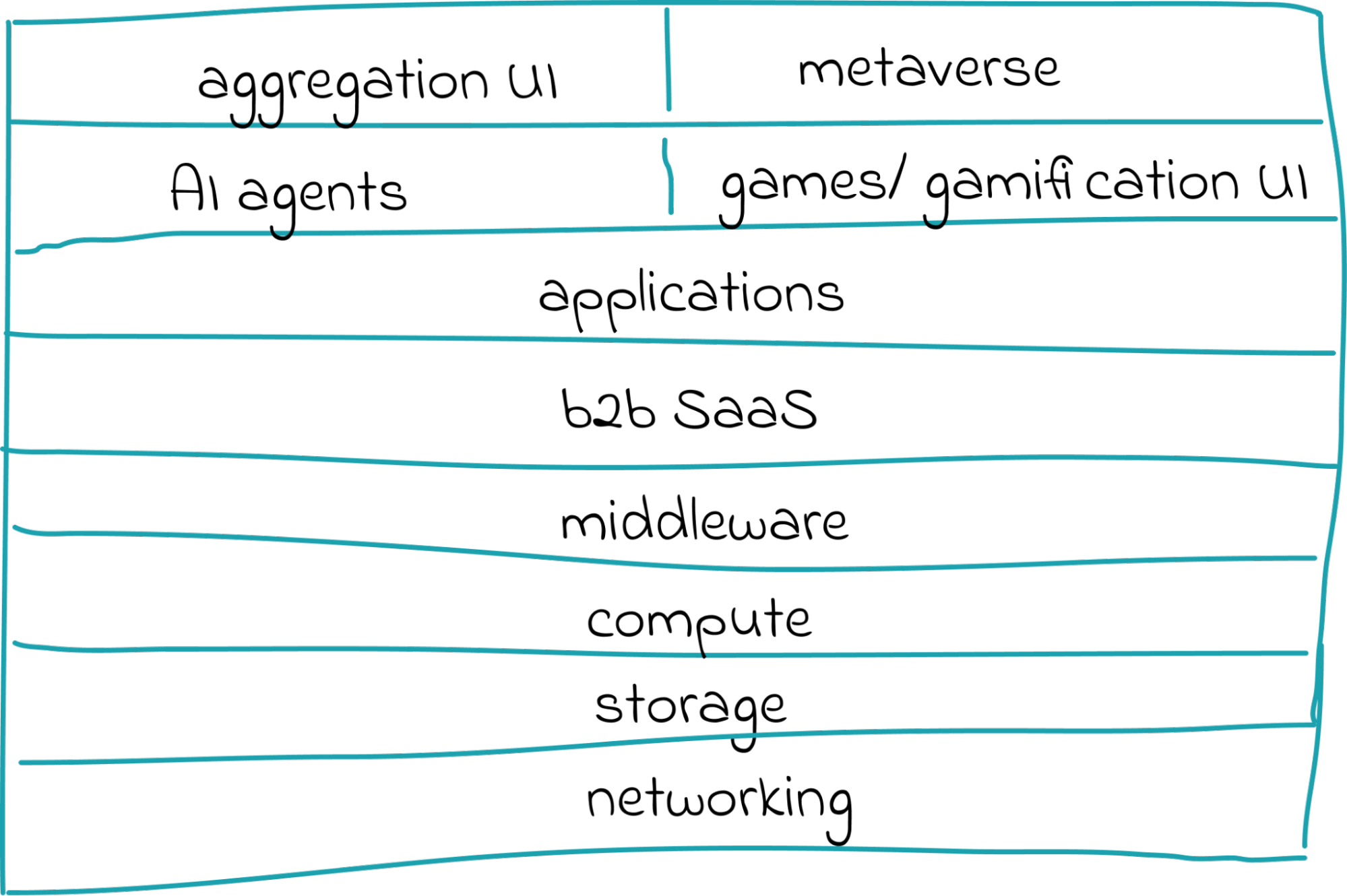

Using the same metaphorical visualization - instead of vertical growth we see Web3 winners grow horizontally as they emerge in their respective categories. And the global value stack is a single homogeneous set of slices stacked vertically into one big tech stack, with each protocol and app being a single slice of that layered body. See a simplified visualization of this below.

Simplified Global [Internet] Value Stack

What does the winner of "storage" category look like in such a scenario? It's the protocol that hosts data for the majority of all of the internet globally - e.g. both in China and US, as well as anywhere else, which means it captures storage portion of the AWS, Alibaba Cloud, Azure, Tencent Cloud, Google Cloud, Hetzner and all other cloud and current "on-prem" storage businesses. Now multiply it by the ever-expanding size of storage needs for the digitized world where AI generates and consumes orders of magnitude more data than we have today and you get a rough idea of the scale such a "thin" layer of value stack may take.

The big question is how do you ensure that the winner in network effects also captures most of the value they create given the open source nature of these technologies? We strongly believe that we are at the very dawn of figuring out the best economics for such systems. Experiments with digital assets that represent access/ownership in these platforms are only just now starting to break out. The quick path to liquidity these tokens take is both a gift and a curse, since it incentivizes people to rush them out the door as soon as possible and make only incremental improvements based on trial and error of earlier iterations. And yet, it is very hard to reverse course for a product that has a token with a "broken" chart. That is why these failures in token economics may cost dearly to builders of even exceptional products.

We are very much of the belief that the big era of token design, a.k.a, the testbed for the most complex and cutting edge econ theory is upon us. We know first hand from economists we work with for portfolio companies how uninspiring a career path in traditional economics is for most of them given little real world output, whereas, on the other hand, there are these closed loop network economies they can implement and constantly tweak.

How We Put Our Framework to Practice

As an investor you want the winner or at least second largest protocol/app serving their respective layer of the stack. We believe that protocols further down the value chain (i.e. towards the very backend of the internet) will be more like one-winner-takes-most common goods. Whereas application layer may have multiple concurrent winners serving different user groups's’ needs, but still ubiquitous within their respective niche.

We don’t know which layer of the stack will be the winning one in terms of capturing most value, moreover – we expect the demand for each service/protocol to be cyclical but "margins" better further up the stack you go (think staples vs consumer discretionary in economic cycles), including middleware (e.g. surge in gaming favors certain middleware more than surge in productivity software). So, you want to own as many category winners as possible and across the stack to have defensibility in your portfolio.

Also, while we don’t know how big each category might get, through heuristics one can probably pick the bigger ones to look for first. We prefer projects in areas that don't feel crowded with competition but make sense both from first principles and founder talent perspectives.

What is key in ensuring you get the winner or close competitor by making sure they create moats/defensibility around them. We believe that in the world of interconnectedness it means network effects first and foremost and strong value capture mechanics secondly. So, as an investor we primarily work with portfolio companies on their composability with other portfolio companies and beyond, while also engineering the most suitable value capture mechanics.

One important thing to note on the network effects is that in the last 20 years of internet growth we've learnt that tech is a popularity contest and not always the absolute best solutions get the most adoption. However, we're of the camp that encourages portfolio teams to have the freedom to not compromise on the technology itself if it's not consumer-facing. It will become much more relevant in the world where integration decisions are driven by AI, which is stripped of human biases and social thinking, when picking the best technology to use. This adds a whole surface of problems to think about, but that's for another time.